|

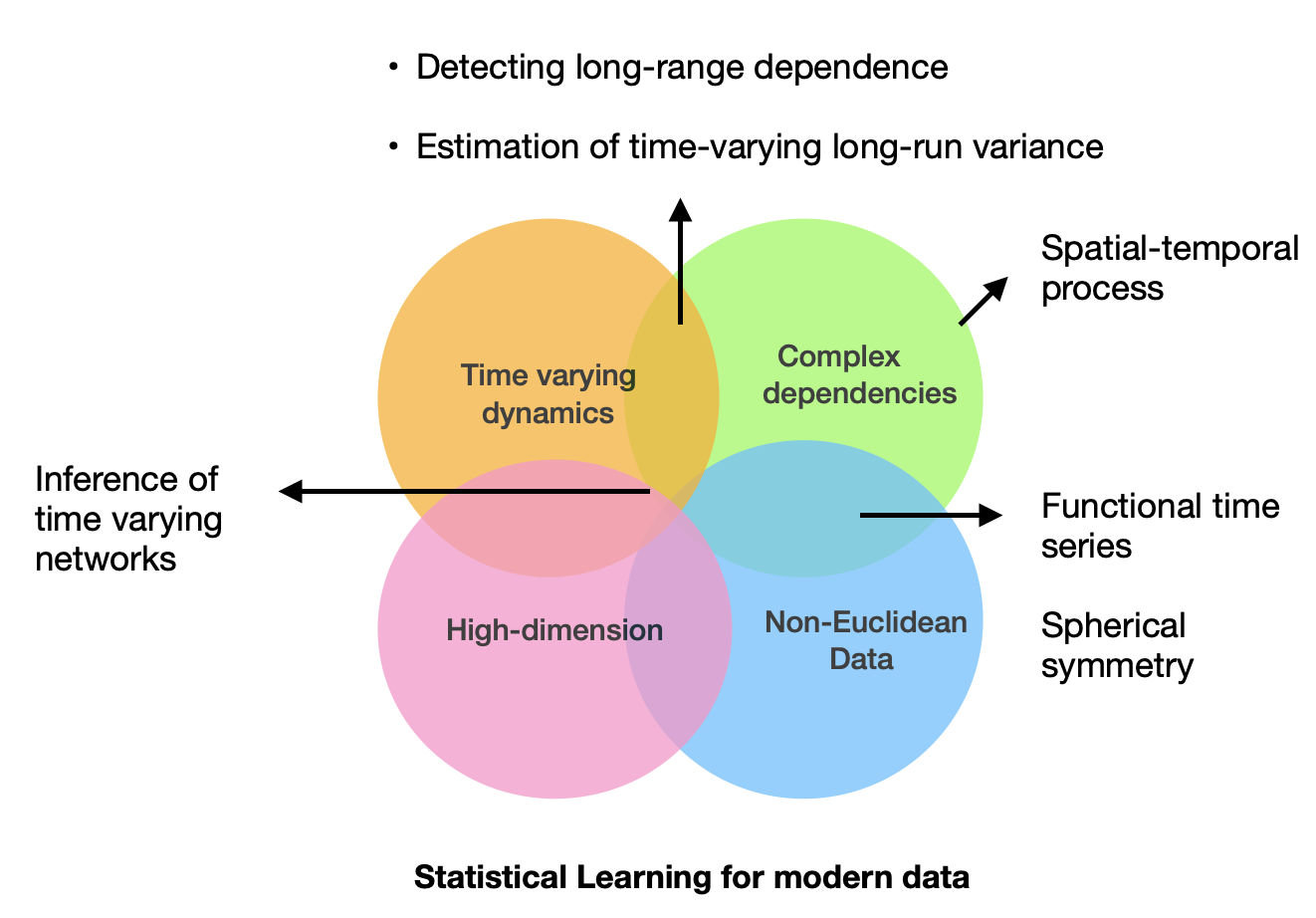

I am currently a postdoc researcher at Department of Mathematics, at Ruhr Unversity Bochum in the group of Holger Dette. I obtained my Ph.d. from Department of Statistics and Data Science at Tsinghua University, Beijing, China, advised by Weichi Wu . In 2020, I obtained my B.Sc. in the School of Statistics and Management, Shanghai University of Finance and Economics. I am broadly interested in statistical learning for complex structure and non-stationary dynamics, see the figure below for an overview. My current research focuses on non-stationary time series, time-varying network, functional time series and long-range dependence. I speak Chinese, English and German as well as Spanish. |

|

|

|

|

|

Lujia Bai*, Holger Dette Preprint (2025+) [arXiv] Most of the work on checking spherical symmetry assumptions on the distribution of the p-dimensional random vector Y has its focus on statistical tests for the null hypothesis of exact spherical symmetry. In this paper, we take a different point of view and propose a measure for the deviation from spherical symmetry, which is based on the minimum distance between the distribution of the vector (‖Y‖,Y/‖Y‖)⊤ and its best approximation by a distribution of a vector (‖Ys‖,Ys/‖Ys‖)⊤ corresponding to a random vector Ys with a spherical distribution. We develop estimators for the minimum distance with corresponding statistical guarantees (provided by asymptotic theory) and demonstrate the applicability of our approach by means of a simulation study and a real data example. |

|

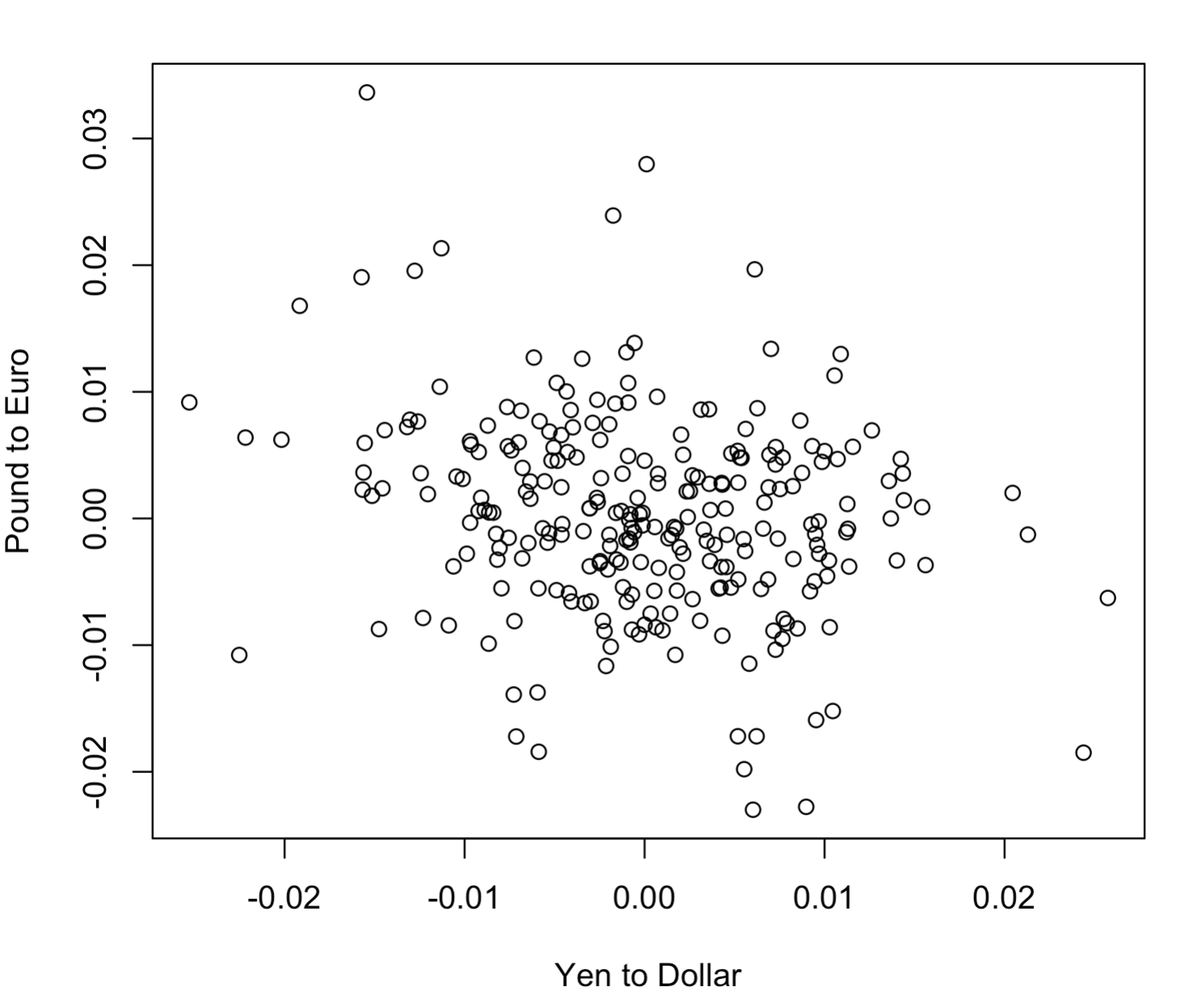

Lujia Bai*, Holger Dette, Weichi Wu Preprint (2025+) [arXiv] In this paper, we introduce a specialized portmanteau-type test tailored for assessing white noise assumptions for multivariate locally stationary functional time series without dimension reduction. |

|

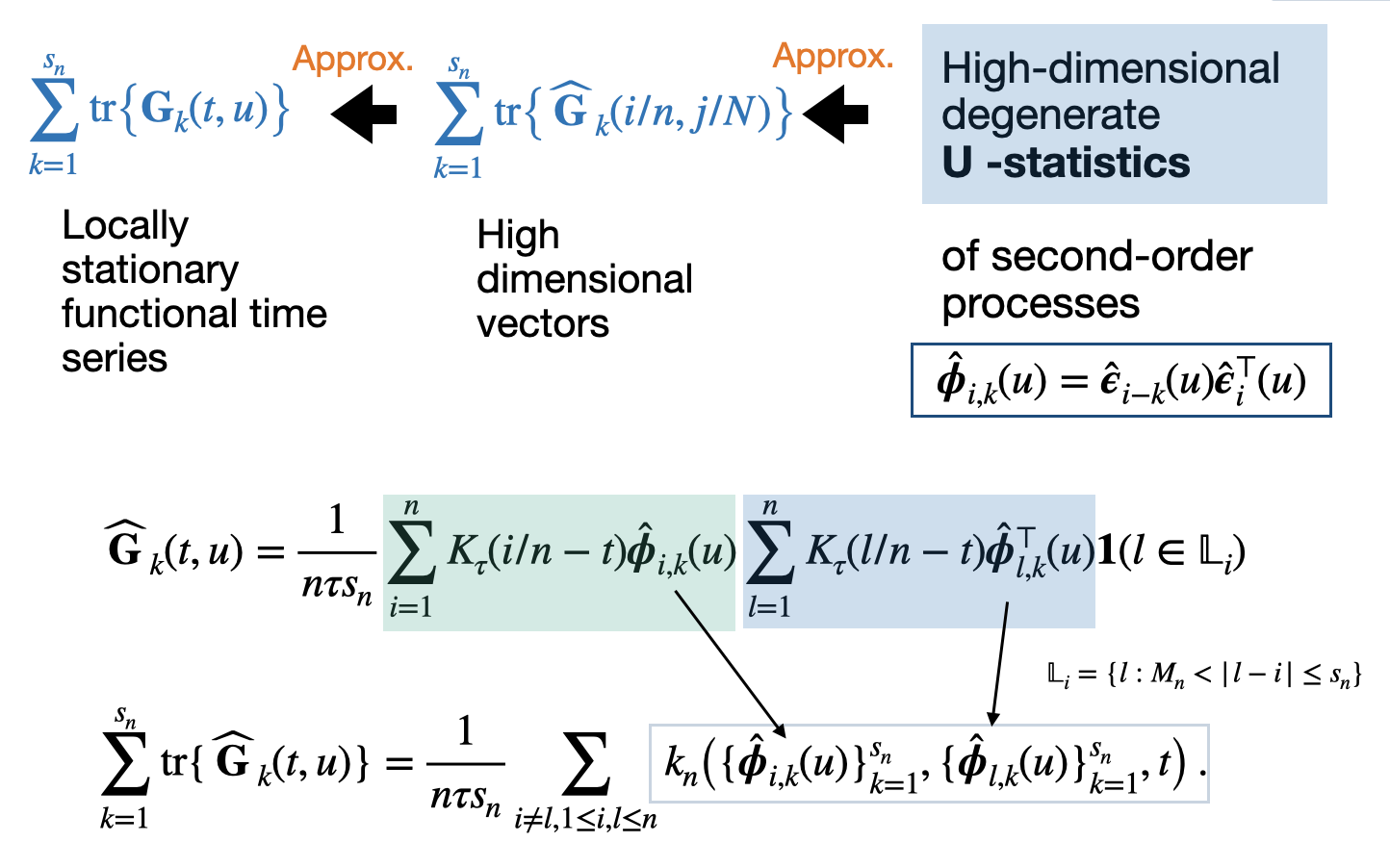

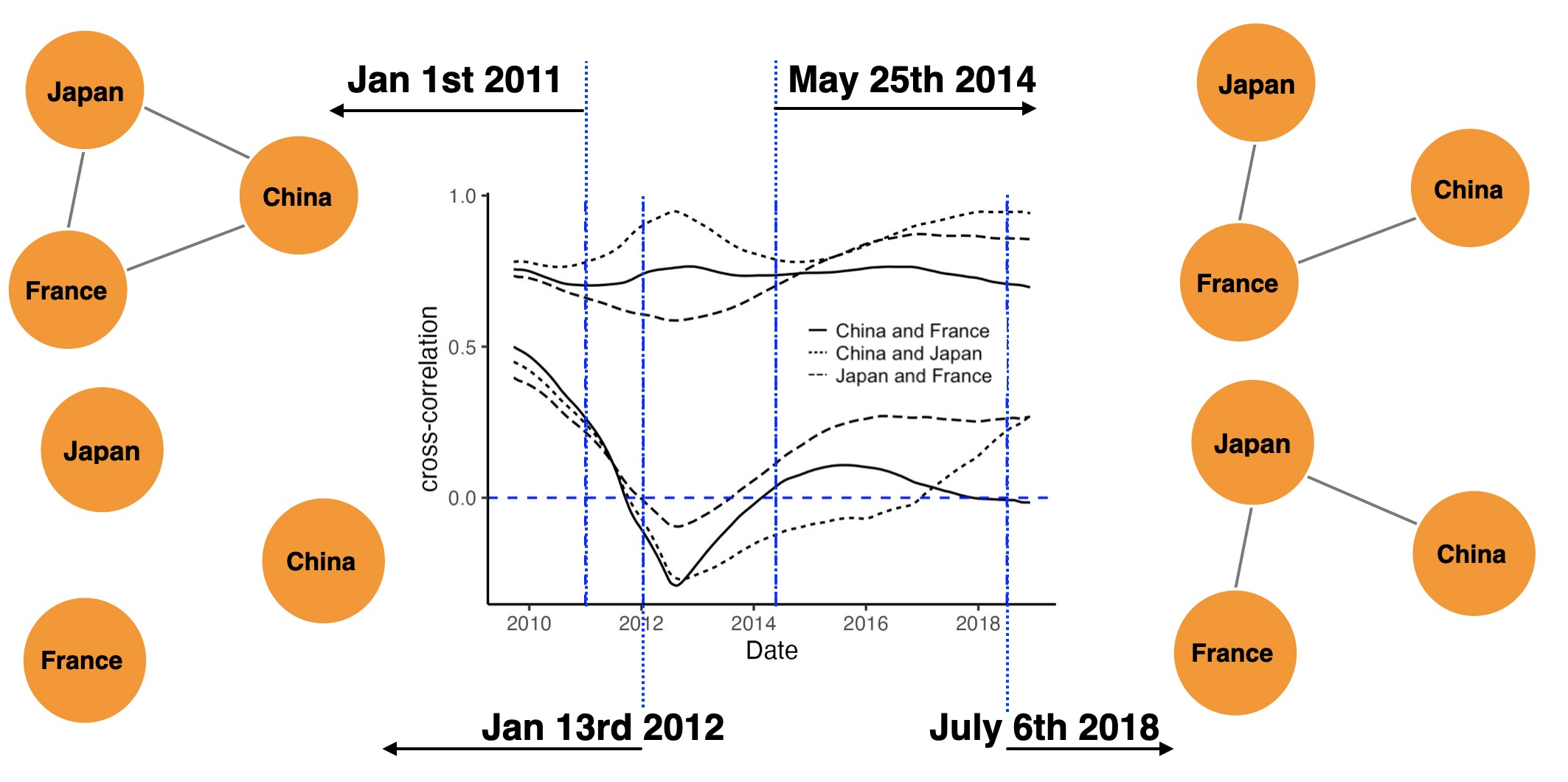

Lujia Bai*, Weichi Wu IEEE Transactions on Information Theory (2025+) [arXiv] [IEEE TIT] This paper proposes a unified framework for inferring large-scale time-varying correlation networks via data-driven time-varying thresholds that can control uncertainty simultaneously. |

|

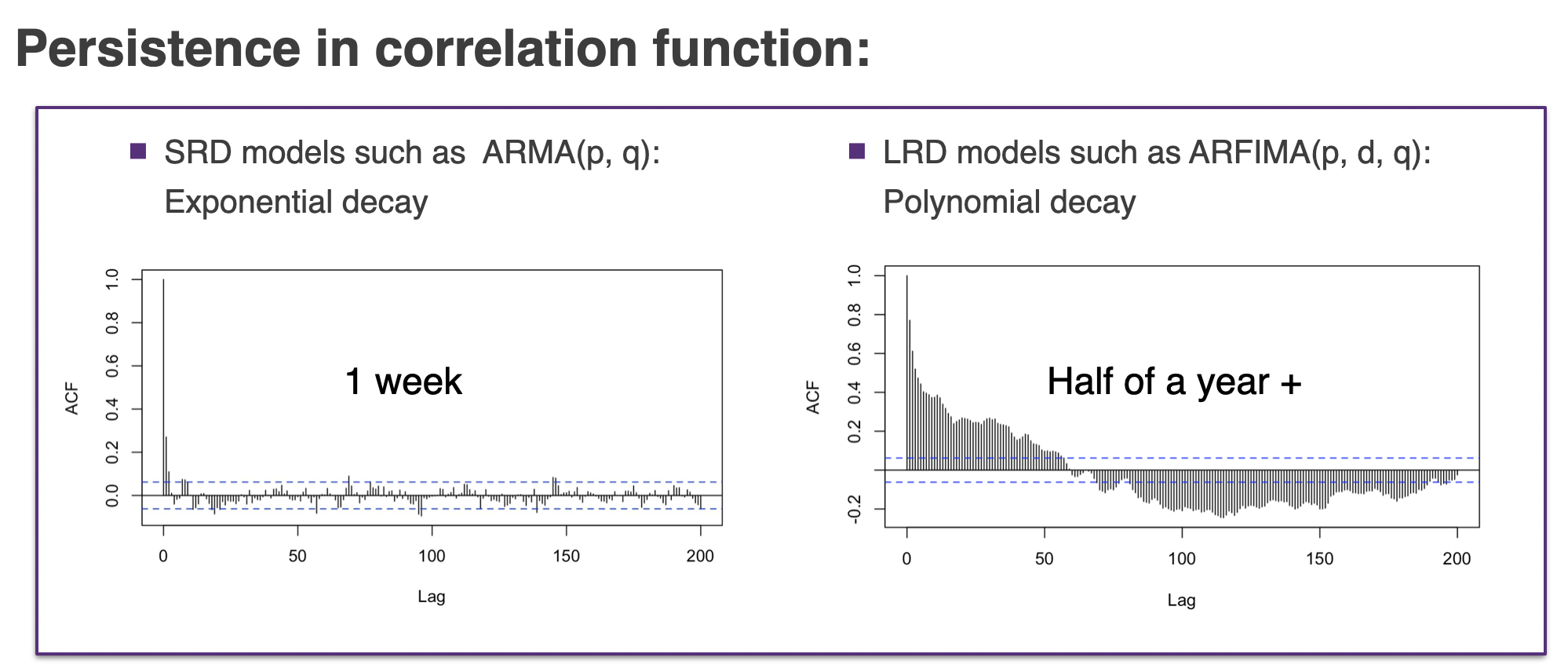

Lujia Bai*, Weichi Wu Bernoulli(2024) [arXiv] [Code] We consider the problem of testing for long-range dependence in time-varying coefficient regression models, where the covariates and errors are locally stationary, allowing complex temporal dynamics and heteroscedasticity. We develop KPSS, R/S, V/S, and K/S-type statistics based on the nonparametric residuals. |

|

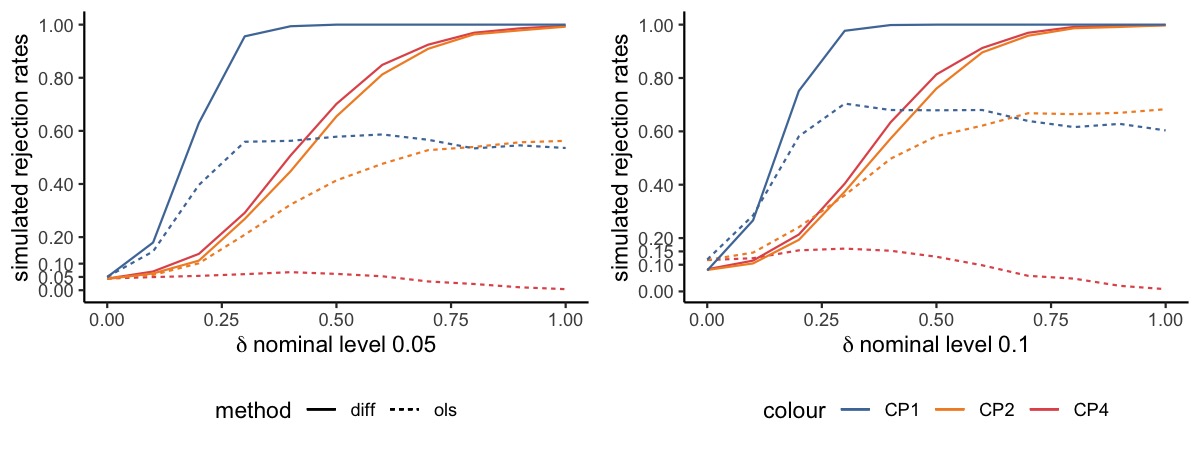

Lujia Bai*, Weichi Wu Biometrika(2024) [arXiv] [Code] We propose a novel difference-based and debiased long-run covariance matrix estimator for functional linear models with time-varying regression coefficients, allowing time series non-stationarity, long-range dependence, state-heteroscedasticity and their mixtures. We apply the new estimator to existing tests, overcoming the notorious non-monotonic power phenomena and improving the performance via the residual free formula. |

|

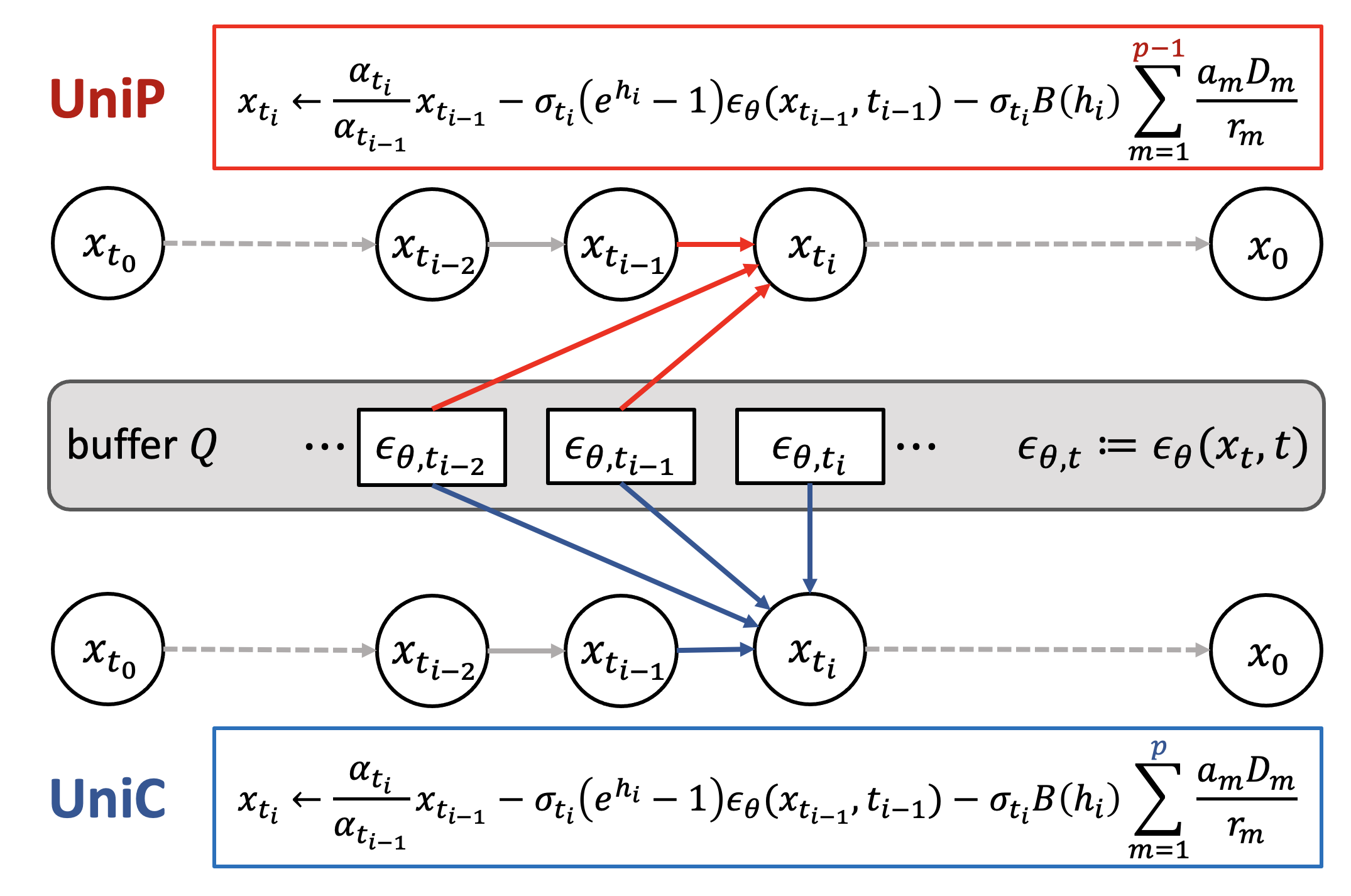

Lujia Bai*, Wenliang Zhao*, Yongming Rao, Jie Zhou , Jiwen Lu NeurIPS 2023 [arXiv] [Code] [Project Page] UniPC is a training-free framework designed for the fast sampling of diffusion models, which consists of a corrector (UniC) and a predictor (UniP) that share a unified analytical form and support arbitrary orders. |

|

|

|

|

|

|

|

|

|

|