|

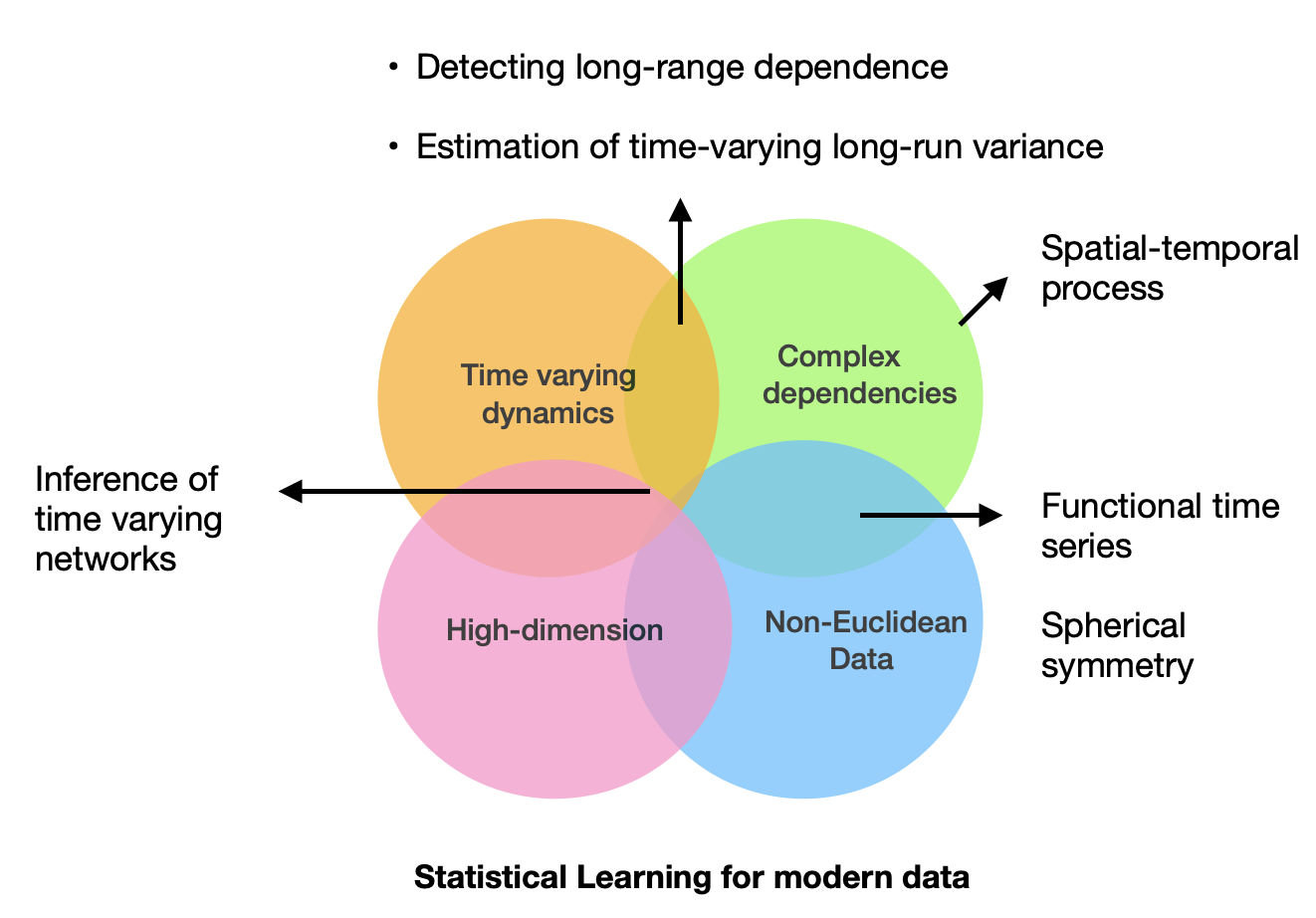

I am currently a postdoc researcher at Department of Mathematics, at Ruhr Unversity Bochum in the group of Holger Dette. I obtained my Ph.d. from Department of Statistics and Data Science at Tsinghua University, Beijing, China, advised by Weichi Wu . In 2020, I obtained my B.Sc. in the School of Statistics and Management, Shanghai University of Finance and Economics. I am broadly interested in statistical learning for complex structure and non-stationary dynamics, see the figure below for an overview. My current research focuses on non-stationary time series, time-varying network, functional time series and long-range dependence. I speak Chinese, English and German as well as Spanish. |

|

|

|

|

|

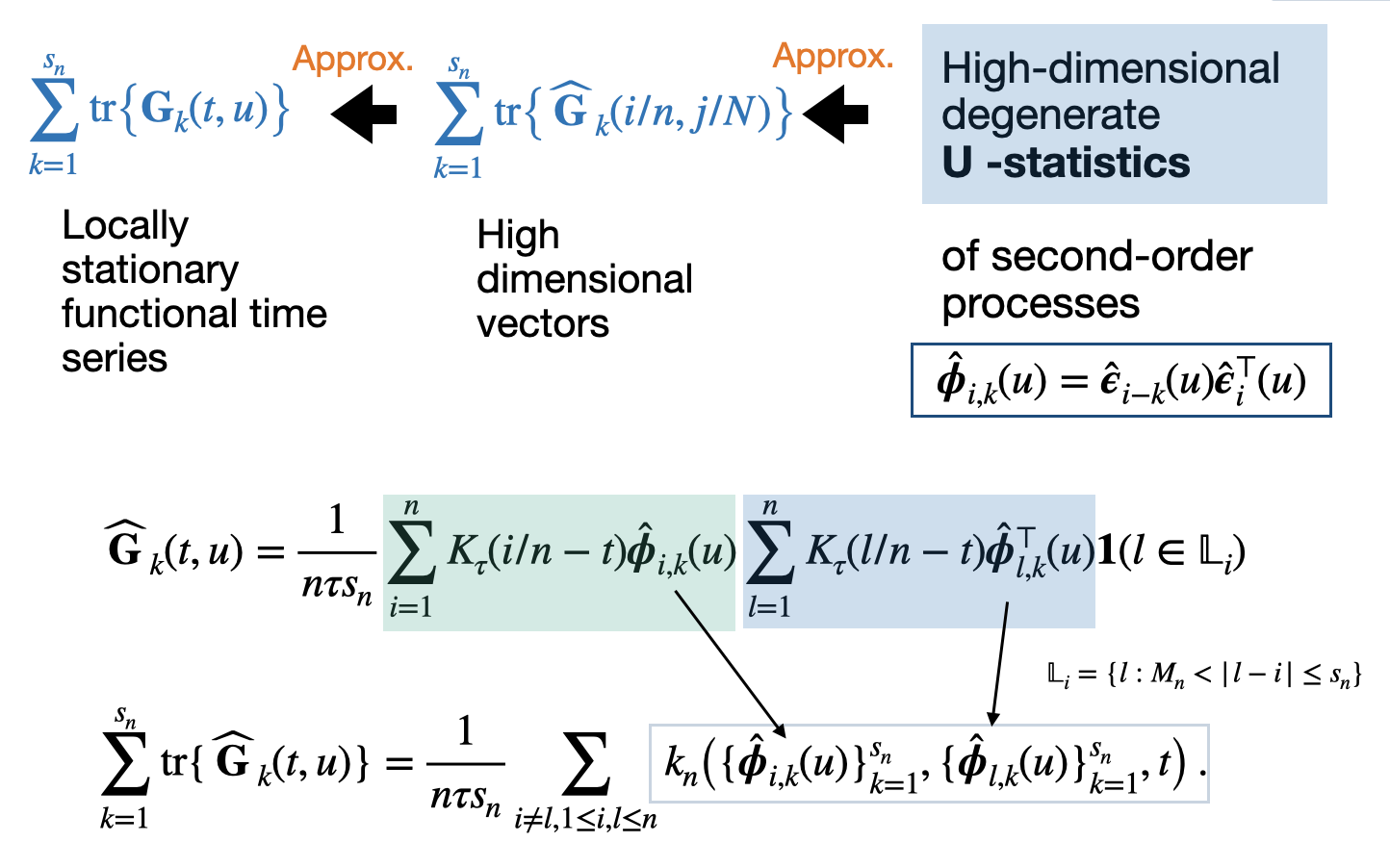

Lujia Bai*, Qirui Hu , Weichi Wu Journal of the Royal Statistical Society Series B: Statistical Methodology (2026+) [JRSSB] We study the problem of detecting and localizing change points for a general class of locally stationary functional time series. To accommodate the nonstationarity and other possible complex features, such as discontinuous trajectories, and heterogeneous partial measurement error of contemporary functional data, we propose methods that do not rest on the preprocessing techniques of presmoothing and dimension-reduction, which would be less accurate without the assumptions of stationarity and continuous trajectories. |

|

Lujia Bai*, David Veitch, Weichi Wu, Wenyang Zhang, Zhou Zhou Preprint (2026) [arXiv] This paper studies high-dimensional trend inference for piecewise smooth signals under nonstationary noise and asynchronous structural breaks by first detecting asynchronous changes without assuming stationarity and then further exploiting latent group structures to estimate trend functions. |

|

Lujia Bai*, Holger Dette, Zihao Yuan Preprint (2026) [arXiv] A crucial assumption to reduce computational complexity in spatial-temporal data analysis is separability, which factors the covariance structure into a purely spatial and a purely temporal component. In this paper, we develop statistical inference tools for validating this assumption for a second-order stationary process under both domain-expanding-infill asymptotics and domain-expanding asymptotics. |

|

Lujia Bai*, Holger Dette Preprint (2025+) [arXiv] Most of the work on checking spherical symmetry assumptions on the distribution of the p-dimensional random vector Y has its focus on statistical tests for the null hypothesis of exact spherical symmetry. In this paper, we take a different point of view and propose a measure for the deviation from spherical symmetry, which is based on the minimum distance between the distribution of the vector (‖Y‖,Y/‖Y‖)⊤ and its best approximation by a distribution of a vector (‖Ys‖,Ys/‖Ys‖)⊤ corresponding to a random vector Ys with a spherical distribution. We develop estimators for the minimum distance with corresponding statistical guarantees (provided by asymptotic theory) and demonstrate the applicability of our approach by means of a simulation study and a real data example. |

|

Lujia Bai*, Holger Dette, Weichi Wu Preprint (2025+) [arXiv] In this paper, we introduce a specialized portmanteau-type test tailored for assessing white noise assumptions for multivariate locally stationary functional time series without dimension reduction. |

|

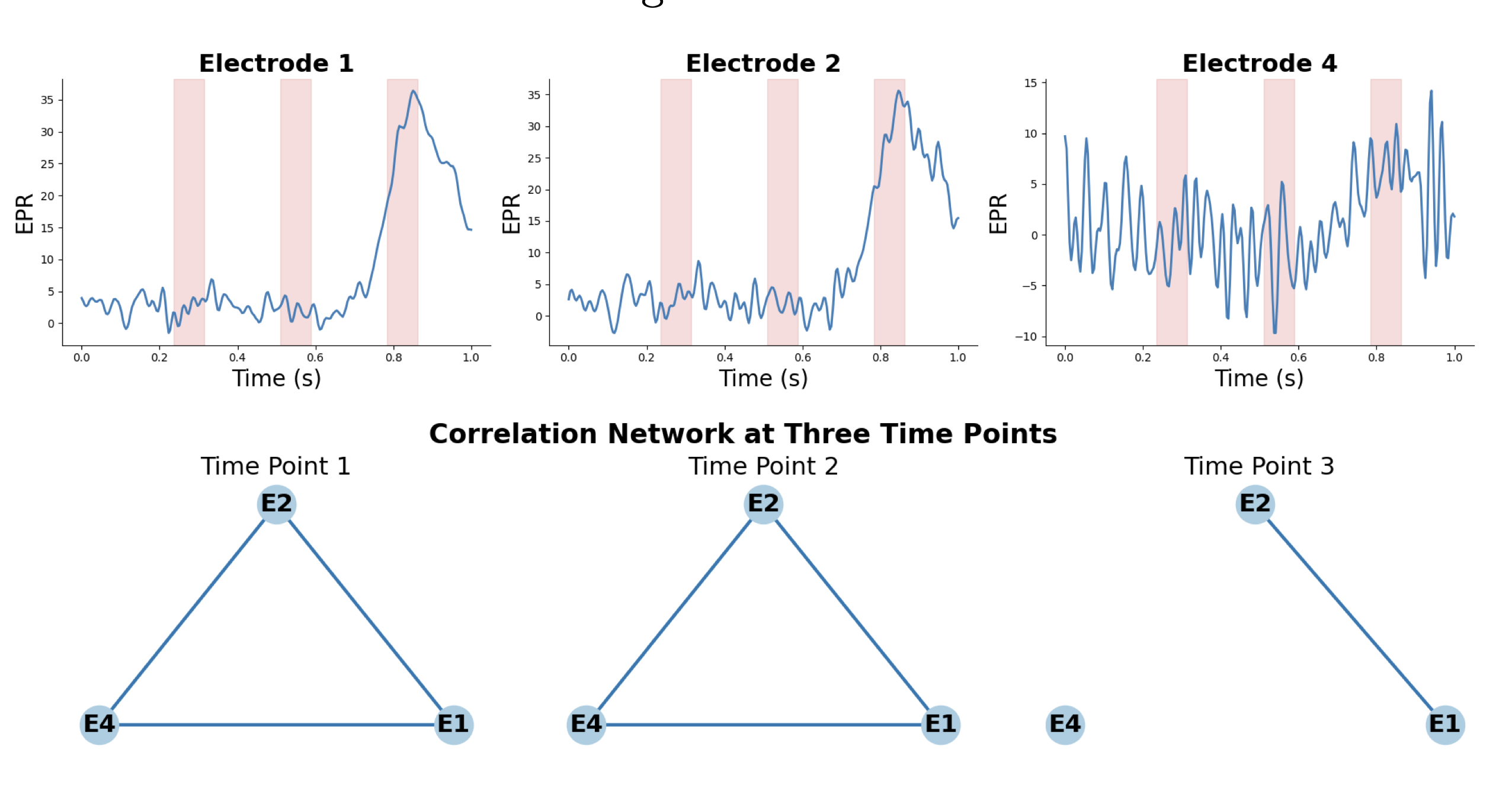

Bufan Li, Lujia Bai*, Weichi Wu Preprint (2025+) [arXiv] This paper presents a systematic framework for uniformly controlling false discovery rate in learning time-varying correlation networks from high-dimensional, non-linear, non-Gaussian and non-stationary time series with an increasing number of potential abrupt change points in means. |

|

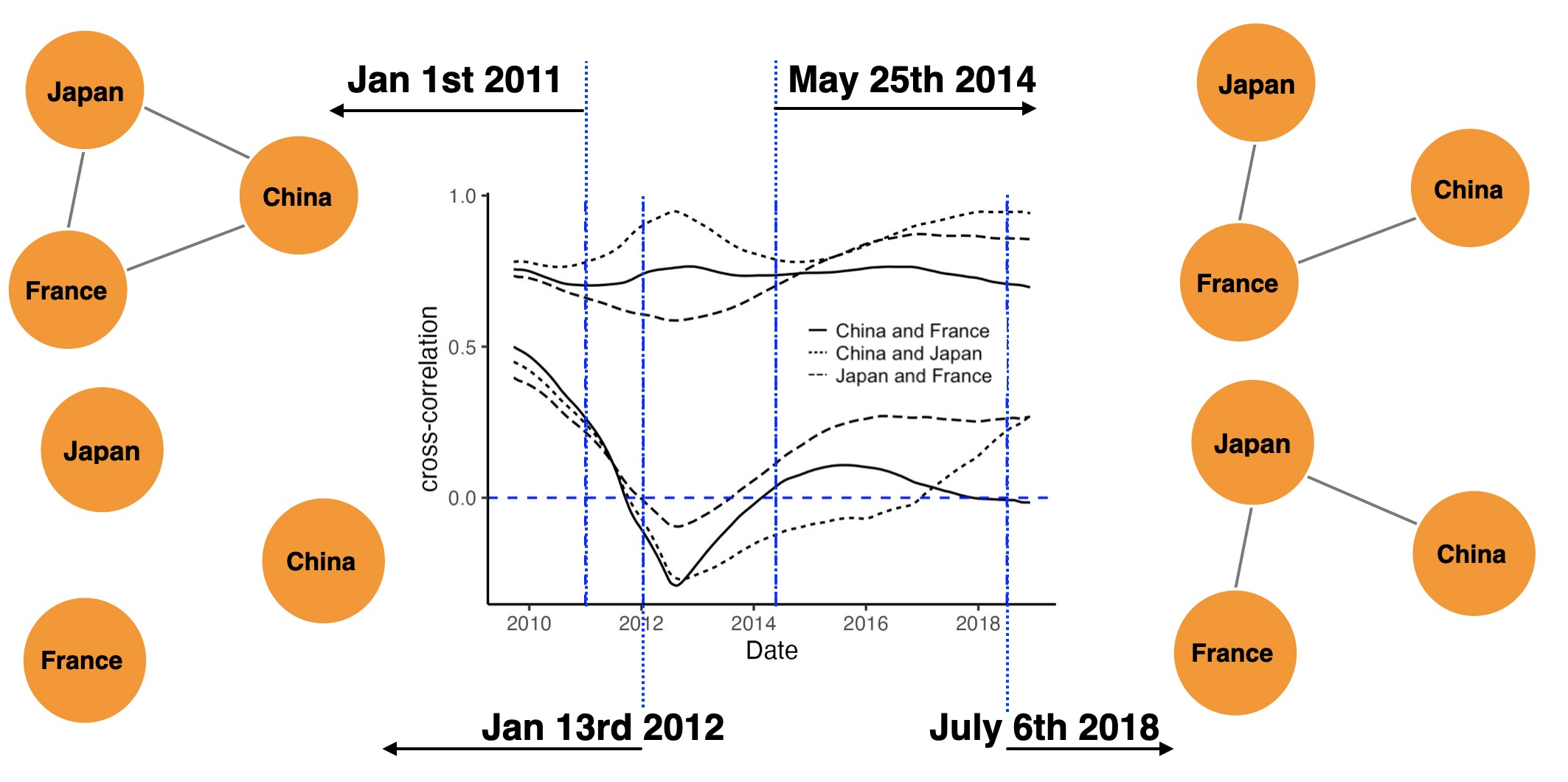

Lujia Bai*, Weichi Wu IEEE Transactions on Information Theory (2025+) [arXiv] [IEEE TIT] This paper proposes a unified framework for inferring large-scale time-varying correlation networks via data-driven time-varying thresholds that can control uncertainty simultaneously. |

|

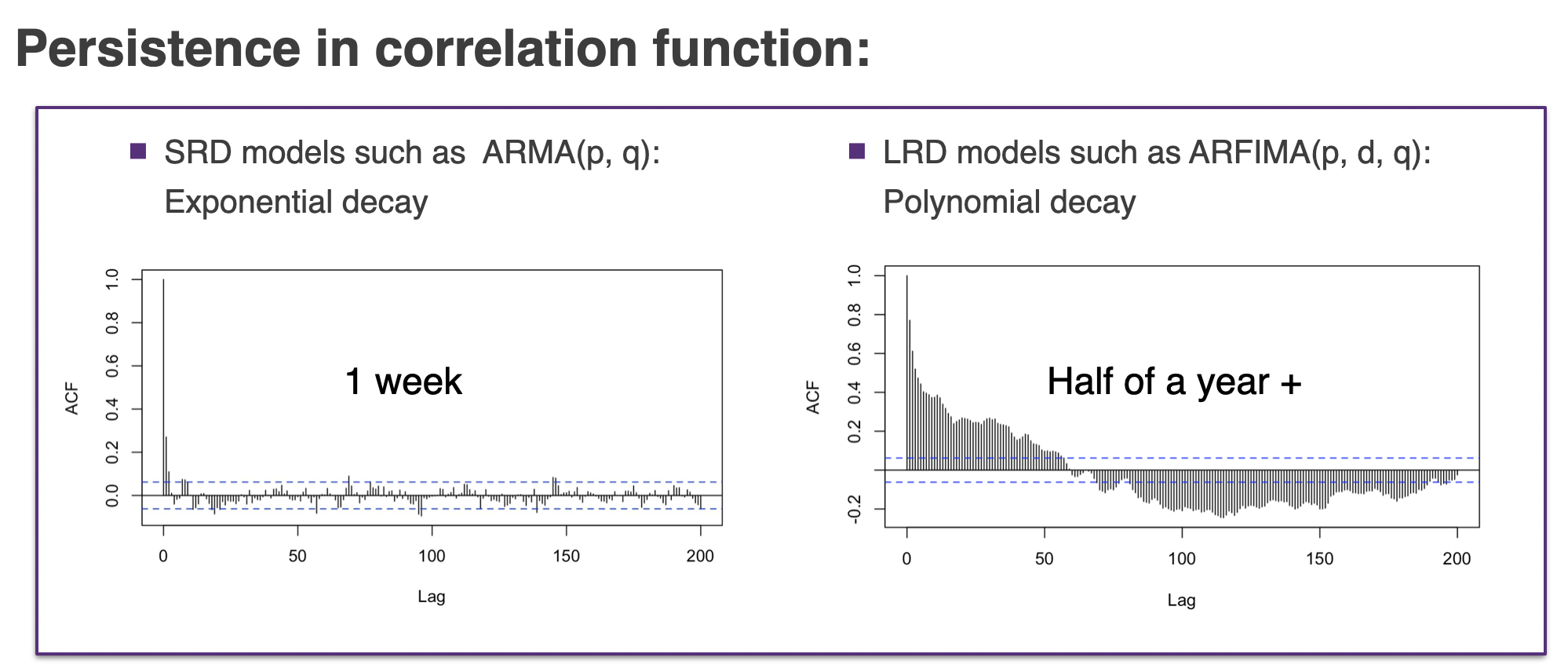

Lujia Bai*, Weichi Wu Bernoulli(2024) [arXiv] [Code] We consider the problem of testing for long-range dependence in time-varying coefficient regression models, where the covariates and errors are locally stationary, allowing complex temporal dynamics and heteroscedasticity. We develop KPSS, R/S, V/S, and K/S-type statistics based on the nonparametric residuals. |

|

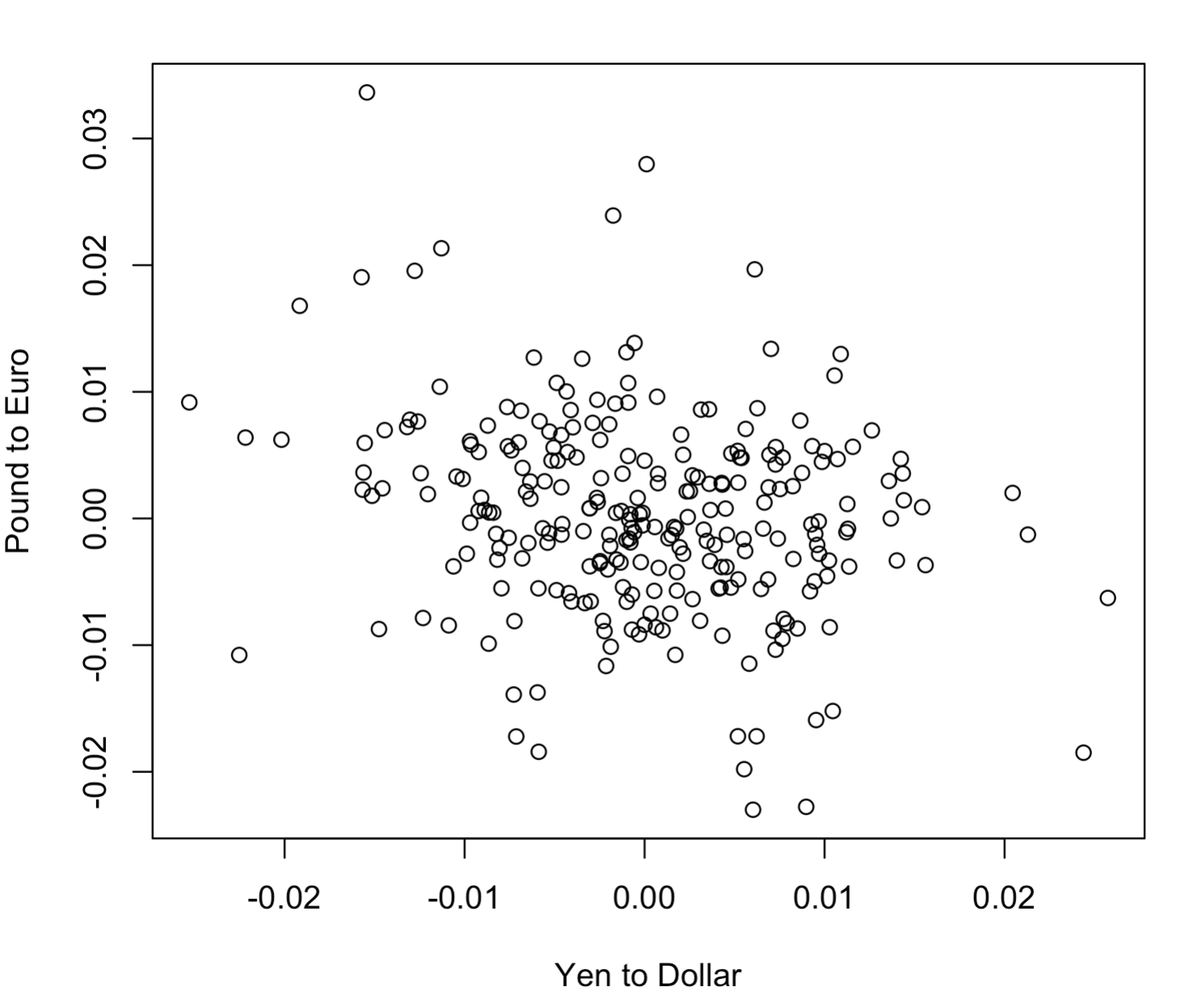

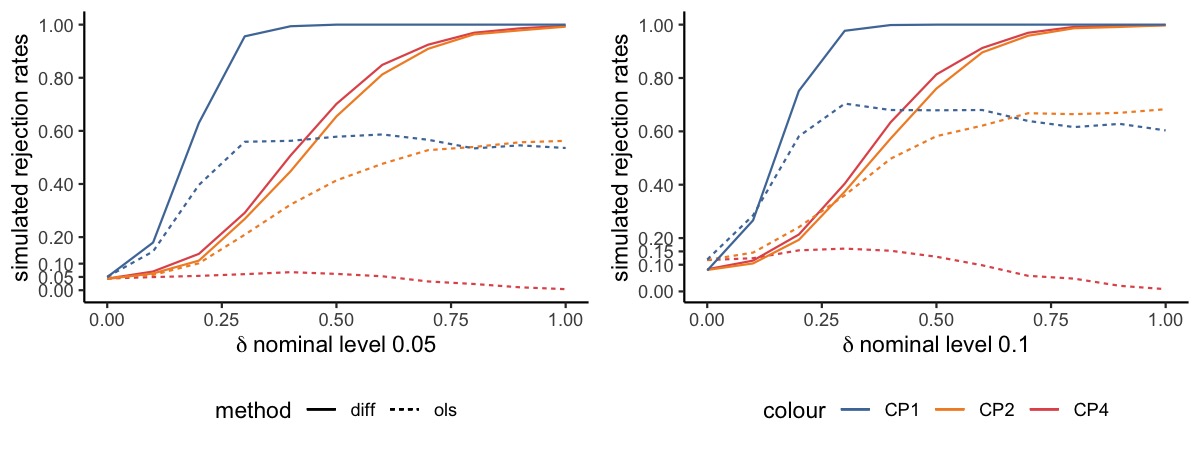

Lujia Bai*, Weichi Wu Biometrika(2024) [arXiv] [Code] We propose a novel difference-based and debiased long-run covariance matrix estimator for functional linear models with time-varying regression coefficients, allowing time series non-stationarity, long-range dependence, state-heteroscedasticity and their mixtures. We apply the new estimator to existing tests, overcoming the notorious non-monotonic power phenomena and improving the performance via the residual free formula. |

|

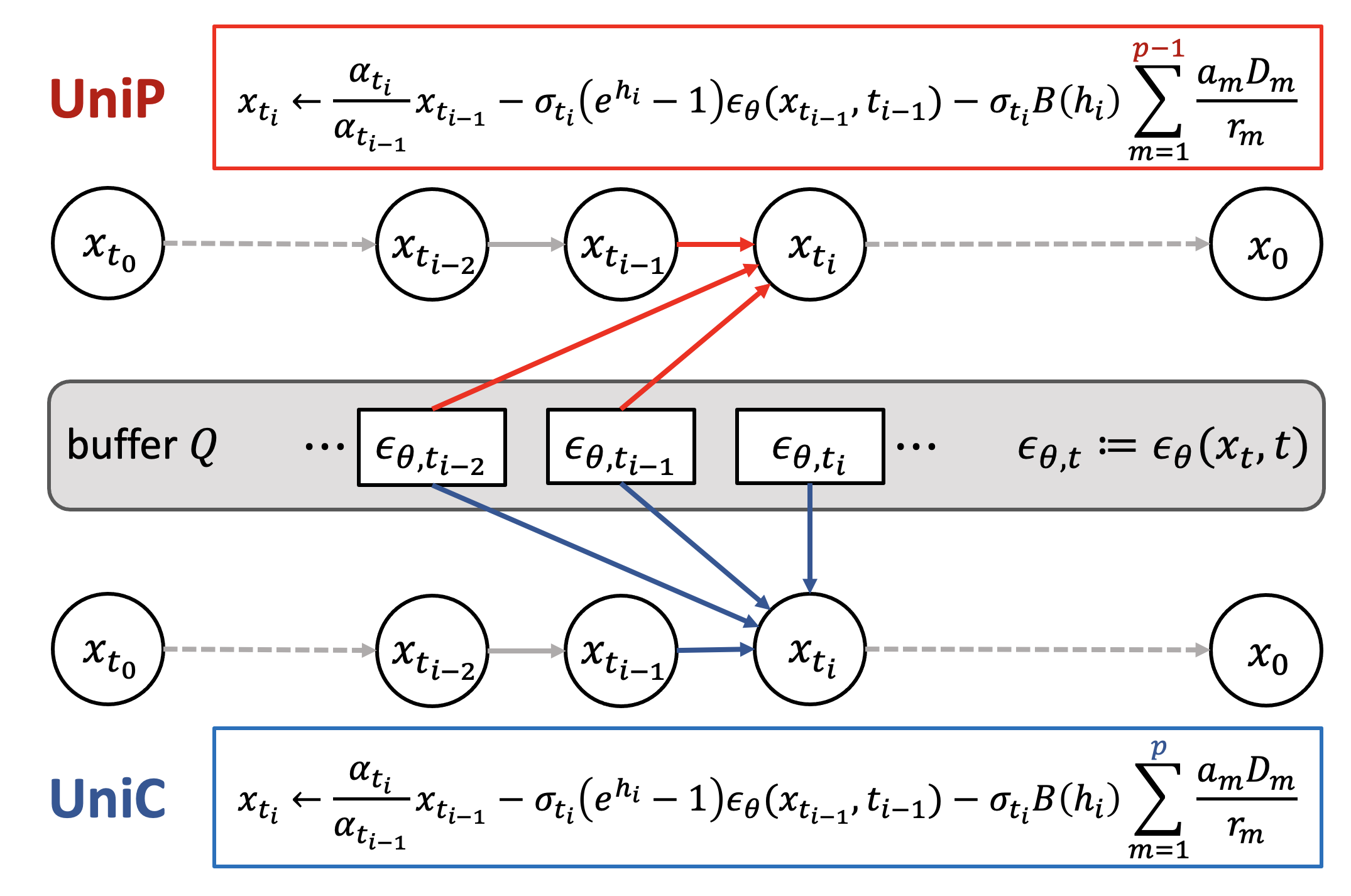

Lujia Bai*, Wenliang Zhao*, Yongming Rao, Jie Zhou , Jiwen Lu NeurIPS 2023 [arXiv] [Code] [Project Page] UniPC is a training-free framework designed for the fast sampling of diffusion models, which consists of a corrector (UniC) and a predictor (UniP) that share a unified analytical form and support arbitrary orders. |

|

|

|

|

|

|

|

|

|

|